MILLIONS of households should brace for more mortgage pain as Spring Statement forecasts spell gloom.

The Office for Budget Responsibility has warned the treasury that inflation is now forecast to peak at 3.8% in July 2025, higher than previous expectations.

This warning comes despite inflation having eased to 2.8% in the 12 months to February, with it unlikely to return to the Bank of England‘s 2% target until the following year.

Such forecasts could prompt the Bank of England's (BoE) Monetary Policy Committee (MPC) to hold off on further interest rate cuts.

Responding to Rachel Reeves‘ remarks on the OBR forecasts during today's Spring Statement, Shadow Chancellor Mel Stride stated: “Inflation, which was down to 2% bang on target on the very day of the last general election under a Conservative government.

“We are now told this year we'll be running at twice the level of the forecast under ourselves in 2024.

“This is going to mean prices bearing down on households and on businesses, right across the country, because of her choices.”

Leaving interest rates unchanged is likely to have a limited immediate impact on those with tracker and variable-rate mortgages, as their interest rates are directly tied to the Bank rate and will remain at current levels.

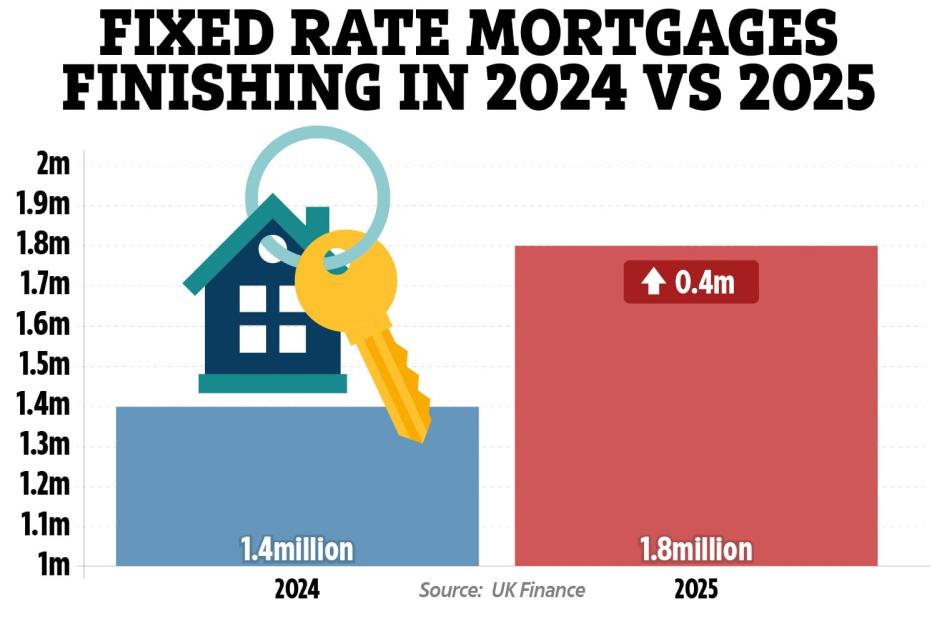

However, delays to BoE rate cuts represent a significant setback for the 1.8million homeowners whose fixed-rate deals are approaching expiry.

These mortgages were secured when interest rates were as low as 2.4%, leaving borrowers facing substantially higher repayment costs when they come to remortgage.

Since then, the BoE base rate has risen sharply, driving up mortgage rates.

Currently, the average two-year fixed-rate mortgage stands at 5.35%, while the typical five-year fixed rate is 5.19%, according to data from moneyfactscompare.co.uk.

To illustrate the impact, borrowers who locked in their deals five years ago benefited from much lower rates, with the average two-year fix at just 2.43% and the five-year fix at 2.74%.

For example, a homeowner with a £300,000 mortgage who secured a five-year fix in 2020 would have paid an average of £1,382 per month.

In stark contrast, the same £300,000 mortgage on a typical five-year fixed rate today would cost £1,787 per month – an increase of £405 each month, or £4,860 over the course of a year.

Those planning to move house from April onwards have also been dealt a significant blow, as Rachel Reeves confirmed in her Spring Statement that the stamp duty holiday, set to end on 31 March, will not be extended.

Key announcements in the Spring Statement:

- No new tax rises:The Chancellor ruled out further tax hikes and pledged to crack down on tax avoidance, aiming to raise an extra £1bn.

- Growth downgraded for 2025:The OBR halved its GDP growth forecast for next year from 2% to just 1%.

- Growth boost from planning reforms: New housing policies expected to raise GDP by 0.6 per cent over the next decade.

- Housebuilding surge: 1.3 million homes expected over five years, with construction hitting a 40-year high.

- £2.2bn extra for defence:Additional funding confirmed to help meet the 2.5 per cent of GDP defence target.

- £400m Defence Innovation Fund: Backing new tech like drones and AI for the front line.

- Welfare shake-up:Targeted employment support and welfare reform to reduce benefit spending.

- Civil service cuts:New voluntary exit schemes and AI tools to shrink Government.

Cut you monthly mortgage payments

Update your mortgage term

When you apply for a new mortgage, repayments are calculated over a set time period which can be anywhere between 20-40 years.

If you are struggling with an increase in bills, one way to lower repayments is to stretch the mortgage term – meaning you are paying off the debt over a longer period of time.

Opting for the longest possible mortgage term will reduce your bills making them more manageable in the short term.

On a £250,000 mortgage and a 5% rate, you'd pay £1,461 a month on a 25-year term.

However, if you increased the term to 35 years you'd pay £1,261 a month if all other factors remained the same. That works out at £200 less a month.

It's important to note that repaying your mortgage over a longer time frame means that you ultimately pay more in interest on the debt.

If you do increase your mortgage term, it's a good idea to bring it back down as and when you can to avoid paying considerably more interest.

Fix your deal for longer

If you’re coming to the end of your mortgage term and are looking to get the lowest possible repayment, it could be worth fixing for longer.

As mentioned above, the two-year is 5.35% compared to 5.19% for a five-year deal, according Moneyfacts.co.uk.

The risk you take is that in two years time, rates could be significantly cheaper leading you to miss out.

However, no one knows what will happen for certain. And taking out a longer fix can help you plan your finances and budgets over a longer term.

A broker should be able to help work out if it's a good idea to fix on a deal for longer.

Overpay your mortgage

If you have spare cash, putting it towards paying more off your mortgage can bring down monthly costs ahead of locking into a new rate.

Over payments go towards eroding the underlying debt of the loan, which is what is used to calculate interest.

A lower outstanding debt means lower interest payments.

In most cases, lenders will let you pay off up to 10% of your total mortgage in one year.

Overpaying could be a good idea if you come into a lump sum of cash.

Or if you can pay even £20 extra a month it will make a difference in the long term.

However, it's important to follow your lender's rules on over payments or you could be hit with an ‘early repayment charge' which can be very costly.

What's happening to interest rates?

Last week, the BoE's rate-setters voted to maintain the base rate at 4.5%.

They last voted to cut rates from 4.75% to 4.5% in February, the third reduction since 2020 and a boon for squeezed borrowers.

But, the latest decision to maintain interest rates comes amid inflation consistently remaining above the Bank of England‘s 2% target, with today's OBR forecast reinforcing this outlook further.

The BoE adjusts its base rate, which influences the interest rates charged to banks, as a tool to manage inflation.

By maintaining the base rate at its current level, the goal is to curb borrowing and spending.

However, striking the right balance between controlling inflation and supporting economic growth remains a challenge.

TheUK economycontinues to struggle, withthe Officefor National Statistics (ONS) reporting that Gross Domestic Product (GDP)unexpectedly shrank by 0.1%in January 2025, contrary to economists' expectations of growth.

The OBR's forecast released today indicates that the UK economy is now expected to grow by just 1% in 2025, a downward revision from its earlier projection of 2%.

Money markets had previously anticipated that the Bank of England would lower interest rates three times in total, reducing them to 4% by the end of the year.

For the time being, the trajectory of future rate cuts remains uncertain.

How to get the best deal on your mortgage

IF you're looking for a traditional type of mortgage, getting the best rates depends entirely on what's available at any given time.

There are several ways to land the best deal.

Usually the larger the deposit you have the lower the rate you can get.

If you're remortgaging and your loan-to-value ratio (LTV) has changed, you'll get access to better rates than before.

Your LTV will go down if your outstanding mortgage is lower and/or your home's value is higher.

A change to your credit score or a better salary could also help you access better rates.

And if you're nearing the end of a fixed deal soon it's worth looking for new deals now.

You can lock in current deals sometimes up to six months before your current deal ends.

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

To find the best deal use a mortgage comparison tool to see what's available.

You can also go to a mortgage broker who can compare a much larger range of deals for you.

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You'll also need to factor in fees for the mortgage, though some have no fees at all.

You can add the fee – sometimes more than £1,000 – to the cost of the mortgage, but be aware that means you'll pay interest on it and so will cost more in the long term.

You can use a mortgage calculator to see how much you could borrow.

Remember you'll have to pass the lender's strict eligibility criteria too, which will include affordability checks and looking at your credit file.

You may also need to provide documents such as utility bills, proof of benefits, your last three month's payslips, passports and bank statements.